This post is to share my thoughts on Agentic AI transforming and disrupting most industries. There are lots of ideas that can be converted to startups, no shortage. Main skill will be execution and distribution, as always, but even more so now with all the AI tools. Small team of technical and industry domain expert and maybe a sales marketing person. But it’s going to be very founder driven, minimal tech and advisory support. Rely on direct customer engagement using the current tools of social media, podcasts, substack, direct reach, etc.

I am more excited than ever, can’t sleep, can’t sit still, too much to do. Taking the positive growth better future mindset will show ideas, possibilities that negative thinking will never grasp. Hope this helps. Will be refining this thought chain with more articles, podcasts, etc.

“The question is no longer whether AI will transform your industry. The question

is whether your startup will lead that transformation — or become a casualty of it.”

PART 1 | THE CURRENT STATE: FROM COPILOTS TO AUTOPILOTS

We have crossed a threshold. And some of the world’s most sophisticated investors

have said so in writing.

Agentic AI refers to autonomous AI systems that perceive goals, plan multi-step

strategies, use tools, remember context across sessions, and execute tasks with

little or no human intervention. This is fundamentally different from a chatbot

that answers questions. An agent does things — searches the web, writes and runs

code, calls APIs, fills forms, drafts contracts, books appointments, monitors

pipelines, and hands off tasks to other specialized agents.

The numbers confirm the momentum:

– Agentic AI startups raised $2.8 billion in H1 2025 alone, with full-year

projections hitting $6.7 billion (Prosus / Dealroom report).

– The broader agentic AI market, valued at ~$30.9 billion in 2024, is growing

at a CAGR of 31–47% depending on the segment tracked.

– By 2026, the total sector has attracted over $24.2 billion in cumulative

venture funding, with 2026 YTD already showing a 142.6% year-over-year

increase (Tracxn, April 2026).

– Deloitte projects that 25% of companies using generative AI will launch

agentic pilots in 2025, growing to 50% by 2027.

– Gartner forecasts that 33% of enterprise software applications will embed

agentic capabilities by 2028 (up from near-zero in 2024).

The pivot from “AI that suggests” to “AI that executes” is not incremental. It is

architectural. And it opens the door for an entirely new generation of startups

to build vertical applications that were previously impossible.

The enabling technology stack making this possible:

– FOUNDATION MODELS: GPT-4o, Claude 3.x/4.x, Gemini — the reasoning core

that crossed the intelligence threshold enabling autonomous action.

– MODEL CONTEXT PROTOCOL (MCP): Anthropic’s open standard — described by

Bessemer as “USB-C for AI” — that lets agents connect standardized tools,

APIs, and data sources with persistent context.

– AGENT-TO-AGENT PROTOCOLS (A2A): Standards enabling multi-agent

coordination, delegation, and specialization at enterprise scale.

– ORCHESTRATION FRAMEWORKS: LangGraph, CrewAI, AutoGen, Akka — managing

state, memory, decision loops, and multi-agent workflow coordination.

– VECTOR DATABASES: Pinecone, Weaviate, pgvector — long-term memory that

makes agents domain-accurate across sessions.

– LLM OBSERVABILITY: LangSmith, etc — the tracing and

evaluation layer that makes production agents trustworthy and improvable.

– MULTIMODAL CAPABILITIES: Voice, vision, image — unified into a single

agent interface that can perceive and act across every human channel.

The window for founders to build category-defining vertical positions in

agentic AI is open right now. Every major VC firm is saying the same thing

with their checkbooks.

PART 2 | THE GREAT DEBATE: CREATIVE DESTRUCTION OR ECONOMIC RENAISSANCE?

Let’s be honest about both sides of this argument. The stakes are too high for

comfortable platitudes — and the VCs themselves are not avoiding it.

THE CASE FOR CONCERN

──────────────────────

The disruption is real, measurable, and already underway:

– The ILO (2025) estimates that over 600 million jobs globally — roughly a

quarter of all employment — are exposed to generative AI effects.

– Goldman Sachs estimates 6–7% of the U.S. workforce faces net displacement

risk, with ~300 million full-time job equivalents globally affected.

– UPS eliminated 20,000 jobs and closed 73 facilities in 2025 after deploying

AI logistics optimization systems. Salesforce cut 4,000 customer service

roles after AI agents began handling ~50% of interactions.

– McKinsey estimates today’s deployed technology could theoretically automate

~57% of current U.S. work hours. Deployment is the limiting factor.

– One forecast from a senior AI operator: “90% of all white-collar corporate

roles I have seen can be automated with current AI models and the right

agent harness.” That is not a fringe view — it is an engineering assessment.

– Entry-level white-collar workers are disproportionately affected. Younger

tech workers (20–30 years old) have seen unemployment rise nearly 3

percentage points since early 2025.

These are not fear-mongering statistics. They describe a real transition that

demands policy attention, reskilling investment, and social safety net reform.

The political consequences — income polarization, geographic displacement,

skills gaps — are legitimate and must be taken seriously by anyone building

in this space.

THE CASE FOR OPTIMISM (AND THE VC CONSENSUS)

──────────────────────────────────────────────

The historical record, economic theory, and the most credible data all point

toward net positive outcomes — and here, the VC community has been unusually

forthcoming and data-driven:

– The WEF Future of Jobs Report 2025 projects 170 million new jobs created

by 2030, offsetting 92 million displaced — a net gain of 78 million.

– ITIF (December 2025): AI created roughly 119,900 jobs in 2024 while only

~12,700 were lost. The ratio is nearly 10:1 in favor of creation.

– Gartner projects that by 2028, AI will create more jobs than it destroys

across the global economy.

– New role categories are emerging at pace: AI trainers, agent orchestration

engineers, prompt engineers, AI ethics officers, data curators, AI product

managers, agent QA specialists, and AI-augmented domain experts across every

professional field.

– Wage premiums have already emerged for workers with demonstrable AI

skills — a powerful market signal about where value is migrating.

– a16z published its “Big Ideas 2026” series, articulating a parallel shift: AI is moving from prompting to execution. Described a world where “interfaces shift from chat to action, design shifts from human-first to agent-readable, and work shifts to agentic execution. AI stops being something you ask, and becomes something that

does.”

– Sequoia notes the best AI startups are achieving “north of $1M in revenue

per employee” — an efficiency ratio that implies massive value creation

per company, generating new economic surface area.

– Bessemer Venture Partners called the same transition from the infrastructure

side in their State of AI 2025 Report: AI is building “Systems of Action” on

top of existing “Systems of Record.” The legacy enterprise software platforms

that store and organize data are being overlaid by AI-native platforms that act

on that data — faster, cheaper, and with compounding capability.

The Jevons Paradox is the key economic insight here: as intelligent automation

becomes cheaper, organizations will do more of it — expanding markets, serving

previously uneconomical segments, and creating new categories of demand for

human judgment, creativity, and oversight. Goldman Sachs estimates AI will

raise U.S. labor productivity by ~15% when fully adopted. That is new economic

surface area, not a zero-sum redistribution.

The honest synthesis: the transition is genuinely painful in the near term,

especially for routine cognitive work. But every general-purpose technology

disruption in history — from steam to electricity to computers to the internet

— has ultimately expanded employment and raised living standards. The speed of

this iteration is different; the fundamental economic dynamic is not.

The obligation of founders building in this space is to create products that

genuinely expand economic value — not merely redistribute it.

SOCIAL AND POLITICAL MULTIPLIER EFFECTS

– Democratization of expertise: Agentic AI makes expert-level services

accessible at near-zero marginal cost. As Sequoia’s Sonya Huang put it:

“We’re entering the Age of Abundance — where AI makes once-scarce labor

available everywhere at near-zero cost.” This is profoundly redistributive.

– Geographic leveling: a16z’s Big Ideas 2026 team notes: “Most of the AI

opportunity lives outside of Silicon Valley.” Companies will use “forward-

deployed motions to discover opportunities hiding inside big, legacy

verticals” — in agriculture, healthcare, logistics, and services sectors

distributed far outside tech hubs.

– Political risk: Rapid displacement without transition support creates

populist pressure. Founders building here carry a responsibility to think

about who benefits and who bears the cost.

– Data center multiplier: Each large data center creates ~1,500 on-site jobs

and generates an estimated 3.5 additional local jobs per direct position

(ITIF). This is real employment at massive geographic scale.

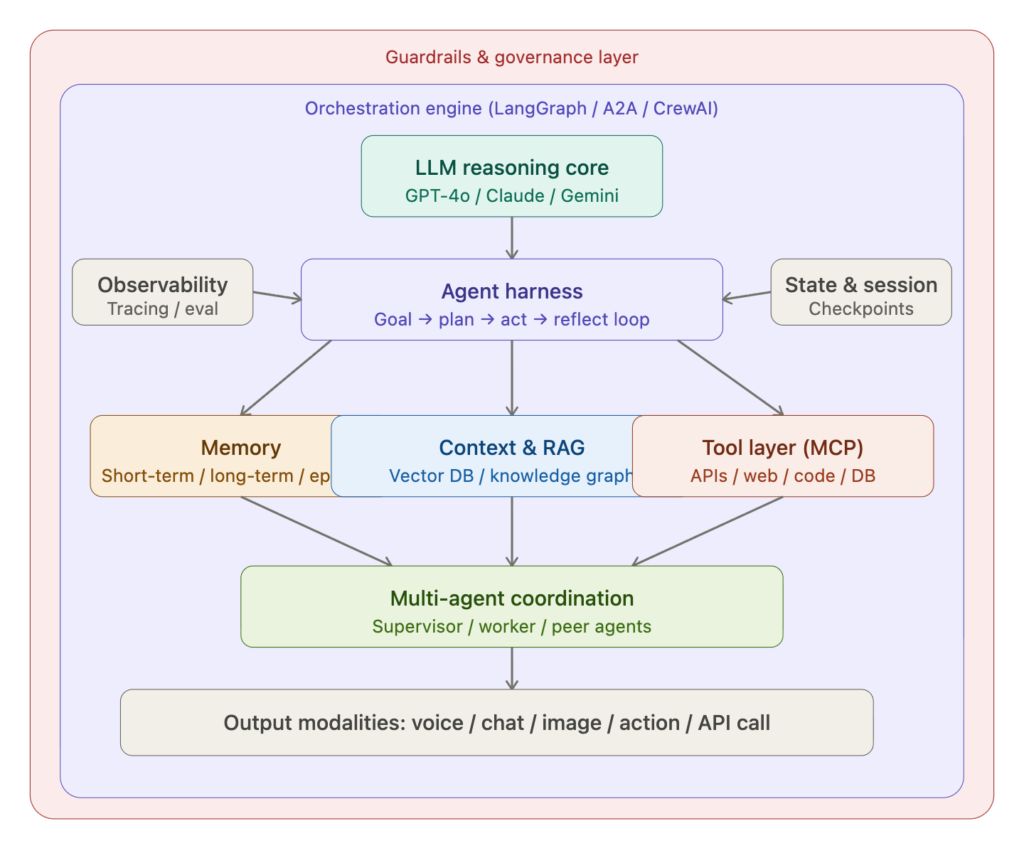

PART 3 | THE ANATOMY OF AN AGENTIC AI SYSTEM

The diagram above maps the generic architecture. Here is what each layer does

and why it matters for startup builders.

– LLM REASONING CORE: The language model (Claude, GPT-4o, Gemini, Llama)

that interprets goals, reasons about context, and generates plans and

outputs.

– AGENT HARNESS (SCAFFOLDING): The control loop wrapping the LLM. Implements

the goal → plan → act → observe → reflect cycle. Agent harnesses /

scaffolding — external engineering layers that work around model

limitations: long-term memory, state handoff, compaction, guardrails, tool

integration, and retry logic.

– MEMORY LAYER (SHORT, LONG-TERM, EPISODIC): Short-term memory holds active

session context. Long-term stores durable facts, preferences, and prior

decisions in vector databases or graph stores. Episodic memory captures

specific experiences for future reference. Bessemer calls this “the key

to the kingdom of enterprise knowledge.”

– CONTEXT & RAG (RETRIEVAL-AUGMENTED GENERATION): Agents dynamically retrieve

relevant knowledge from vector databases, knowledge graphs, and structured

data. Enterprises need “a continuous way to clean, structure,

validate and govern their multimodal data so downstream AI workloads

actually work.”

– TOOL LAYER (MCP): The action interface — connecting agents to APIs,

databases, web browsers, code execution environments, and legacy systems.

Bessemer describes MCP as “a universal specification for AI agents to

access external APIs, tools, and data persistently. Think of it as USB-C

for AI.” This layer is where agents stop being “smart chatbots” and start

being “digital workers.”

– MULTI-AGENT COORDINATION (A2A): Complex tasks decompose across specialized

agents. Enterprises will need systems of coordination:

new layers to manage multi-agent interactions, adjudicate context, and

ensure reliability across autonomous workflows.”

– OBSERVABILITY: Full tracing of every decision, tool call, and failure. Use-case-specific evals built on proprietary

data” — not public benchmarks

– STATE & SESSION MANAGEMENT: Checkpointing enables long-running tasks,

human-in-the-loop approval gates, and graceful failure recovery. Sequoia’s

long-horizon agent framework requires this as a core capability

– GUARDRAILS & GOVERNANCE: The outermost layer. Input/output filtering, prompt

injection detection, tool access controls, content safety, and audit logging.

In regulated industries, this is table stakes.

– OUTPUT MODALITIES: Voice, chat, image, action, and API call — unified.

The browser will emerge as a dominant interface for agentic AI, with voice-first AI products running and optimizing critical parts of every business.

Your competitive moat is NOT the model.

It is the domain expertise, workflow depth, proprietary memory, and the trust

required to operate autonomously in consequential business processes.

PART 4 | INDUSTRY-BY-INDUSTRY: WHERE THE STARTUPS WILL BE BUILT

──────────────────────────

HEALTHCARE & PHARMACY

──────────────────────────

The industry has two problems: administrative overload killing clinicians, and

access barriers killing patients. Agentic AI solves both. Targeting

a specific high-friction workflow with deep AI automation. The global AI in healthcare market is growing from $20.9B (2024) to $148.4B by 2032 at a CAGR of 27.1%.

STARTUP IDEAS:

– Autonomous prior authorization agent: Navigates payer portals, assembles

clinical justification, and submits on behalf of physicians — eliminating

a process costing U.S. healthcare $35B annually.

– Clinical documentation agent: Listens to provider-patient conversations,

generates structured SOAP notes, codes ICD-10 and CPT, files into the EHR.

Ambience Healthcare ($243M, a16z-backed) leads this category.

– Medication adherence companion: Voice agent that proactively checks in

with patients, answers drug interaction questions, refills prescriptions,

and escalates non-adherence to care teams.

– Rare disease diagnostic navigator: Multi-agent system ingesting case

history, literature, and genomic data to surface differential diagnoses —

a genuine second opinion at machine speed.

– Pharmacy benefit negotiation agent: Analyzes formularies, rebate

structures, and utilization patterns to autonomously identify switching

opportunities and generate PBM negotiation briefs.

WHY IT MATTERS: healthcare AI systems operate in a regulated,

high-trust environment — making the compliance layer itself a structural moat

that a new model version cannot dissolve overnight.

──────────────────────────

BANKING & FINANCIAL SERVICES

──────────────────────────

The $1 trillion opportunity is in the legacy back office — KYC, compliance, underwriting,

treasury operations.

Harvey raised $200M at an $11B valuation (led by GIC and Sequoia, March 2026)

— confirming that AI autopilots in professional services command premium

multiples when the domain data moat is real.

STARTUP IDEAS:

– KYC / AML compliance agent: Continuously monitors transactions, cross-

references sanction lists, flags anomalies, generates SAR narratives, and

maintains audit trails — replacing entire compliance operations teams.

– Loan origination orchestrator: End-to-end agent that collects documents,

verifies income and identity, runs credit models, assembles underwriting

packages, and routes for decision — reducing origination cycles from weeks

to hours. JPMorgan reports nearly 30% reduction in consumer banking

servicing costs from its 100+ generative AI tools.

– Treasury and liquidity management agent: Monitors real-time cash positions,

executes sweep transactions, optimizes FX hedges, and surfaces liquidity

forecasts for CFO review.

– Wealth planning agent: Builds personalized financial plans, rebalances

portfolios within defined risk parameters, and identifies tax loss

harvesting opportunities — delivering private wealth management quality

to the mass affluent market.

──────────────────────────

PAYMENTS & FINTECH

──────────────────────────

STARTUP IDEAS:

– Agentic payment rails: Purpose-built infrastructure for agent-to-agent

transactions, with verifiable identity, stablecoin settlement, and

millisecond latency. This is the financial plumbing of the machine economy.

– SMB financial operations agent: Accounts payable, receivable, reconciliation,

and cash flow forecasting run autonomously for small businesses that cannot

afford a finance team.

– Fraud detection and chargeback agent: Real-time transaction analysis,

fraud ring pattern detection, automated dispute response — deployed at

machine speed, not human speed.

– Cross-border payment optimization agent: Analyzes FX rates, correspondent

banking routes, and regulatory requirements in real time for optimal

international payment routing.

──────────────────────────

LOGISTICS & SUPPLY CHAIN

──────────────────────────

Logistics is a prime vertical for “AI-native industrial” companies: logistics companies that deploy AI agents to execute work (not just advise) will dramatically undercut traditional

3PLs and freight brokers.

STARTUP IDEAS:

– Dynamic route optimization agent: Ingests real-time traffic, weather,

border crossing times, and driver HOS data to continuously re-optimize

last-mile and long-haul routes.

– Supplier relationship management agent: Monitors supplier performance,

proactively identifies risk (geopolitical, financial, quality), negotiates

contract renewals, and manages alternative sourcing.

– Customs and trade compliance agent: Prepares and files import/export

documentation, classifies goods under HS codes, calculates duties, and

monitors regulatory changes across jurisdictions.

– Demand sensing and inventory agent: Integrates POS data, external signals,

and promotional plans to autonomously adjust replenishment orders across

a distribution network.

──────────────────────────

AGRICULTURE & AGRITECH

──────────────────────────

The democratization of agronomic expertise via voice-native agentic AI could

have the single largest human impact of any vertical application.

STARTUP IDEAS:

– Crop health monitoring agent: Ingests satellite imagery, drone data, and

soil sensor readings to autonomously identify disease outbreaks, nutrient

deficiencies, and irrigation needs — and execute interventions.

– Precision farming orchestrator: Coordinates autonomous machinery based on

real-time field conditions and agronomic models.

– Agricultural extension agent: Delivers expert agronomic advice in local

languages via voice to smallholder farmers who have never had access to a

trained agronomist. This is the “Age of Abundance” thesis applied to the

500 million smallholder farming families feeding 70% of the developing world.

– Commodity trading and risk agent: Monitors futures markets, weather models,

and crop yield forecasts to advise on hedging strategies for farm operators

and grain cooperatives.

──────────────────────────

ENERGY & UTILITIES

──────────────────────────

The energy transition creates massive compliance, permitting, and operations complexity —

precisely what agentic AI systems can absorb.

STARTUP IDEAS:

– Grid balancing and demand response agent: Autonomously manages energy

dispatch, storage charging/discharging, and demand response programs to

optimize cost and reliability across a distributed grid.

– Renewable energy project development agent: Handles permitting research,

interconnection queue monitoring, environmental impact assessment drafting,

and landowner outreach for utility-scale solar and wind projects.

– Energy audit and efficiency agent: Analyzes smart meter data, building

management system logs, and equipment telemetry to autonomously identify

efficiency opportunities and generate actionable upgrade plans.

──────────────────────────

REAL ESTATE

──────────────────────────

Documents, communications, compliance, and negotiation are all language-dense

— exactly what frontier models now handle well.

STARTUP IDEAS:

– Property acquisition agent: Scans listings, runs comparative market

analysis, models returns, flags zoning and title issues, and schedules

inspections — compressing due diligence from weeks to hours.

– Lease abstraction and management agent: Extracts key terms from commercial

leases, monitors critical date calendars, and manages landlord-tenant

communications.

– Construction project oversight agent: Monitors RFI queues, submittal logs,

schedule updates, and budget variances — proactively surfacing risks and

generating owner reports.

– Real estate lead qualification agent: Voice-native agent handling inbound

buyer and seller inquiries, qualifying intent, and booking appointments.

Voice AI delivers 60–80% cost reduction vs. human call center agents

(Presta, 2026).

──────────────────────────

E-COMMERCE & RETAIL

──────────────────────────

Agentic AI products that learn individual preferences and improve with every interaction, building natural retention and data moats that cannot be replicated by a new model version.

STARTUP IDEAS:

– Autonomous merchandising agent: Monitors sales velocity, competitive

pricing, inventory levels, and margin targets to autonomously adjust

assortment, pricing, and promotional spend.

– Personalized shopping agent: Understands individual customer style, size,

budget, and occasion context to proactively surface relevant products.

– Returns and reverse logistics agent: Manages the full return lifecycle —

label generation, inspection coordination, restocking decisions, refund

processing, and fraud flagging.

– Supplier onboarding agent: Automates the end-to-end supplier qualification

process — document collection, financial verification, compliance screening,

and ERP setup.

──────────────────────────

TECHNOLOGY SERVICES & IT

──────────────────────────

STARTUP IDEAS:

– Autonomous software development agent: Reads requirements, writes code,

generates tests, identifies bugs, and opens pull requests.

– IT operations and incident response agent: Monitors infrastructure alerts,

diagnoses root causes, executes playbooks, and coordinates escalation —

reducing MTTR from hours to minutes.

– Security operations agent: Hunts threats, analyzes logs, correlates signals

across SIEM sources, and generates remediation playbooks autonomously.

a16z’s Joel de la Garza identifies security as a prime vertical: “AI will

automate repetitive cybersecurity tasks, closing the long-standing hiring

gap and freeing security teams for high-value work.”

– Technical documentation agent: Maintains living documentation by monitoring

code changes, API updates, and architectural decisions — always current,

never outdated.

──────────────────────────

CALL CENTERS & CUSTOMER SERVICE

──────────────────────────

This is where agentic AI has moved furthest, fastest. The economics are overwhelming:

$/hour per human agent vs. $ per conversation for a voice AI agent, high cost reduction.

STARTUP IDEAS:

– Domain-specific voice agent: Trained specifically for dental practices, law

firms, HVAC companies, or property managers — domain specialization is the

defensibility. Generic solutions cannot compete.

– Escalation intelligence agent: AI handles Tier 1 resolution autonomously

while routing complex, emotional, or high-value interactions to skilled

human agents with full context pre-loaded.

– Customer success monitoring agent: Proactively monitors usage patterns,

identifies churn risk, triggers outreach, and surfaces expansion

opportunities to account managers.

──────────────────────────

OTHER HIGH-POTENTIAL VERTICALS

──────────────────────────

LEGAL: The entire structure of legal services is being renegotiated.

EDUCATION: Building AI tutors adapting to each

student’s pace in real time. The 1:1 tutoring model that human staffing

ratios make impossible at scale is now achievable via agents.

GOVERNMENT: Government agentic AI is large, slow-moving, and enormously defensible once established.

HR & TALENT: Autonomous recruiting, onboarding coordination, employee

experience monitoring — replacing the most administrative-intensive HR

functions.

INSURANCE: Underwriting agents ingesting satellite imagery, claims history,

and social data to price risk and generate policy documents. WithCoverage

is named by Sequoia as an example of the “autopilot” model working.

PART 5 | THE BUSINESS CASE: WHAT AGENTIC AI ACTUALLY DELIVERS

The commercial case is not speculative. It has a clear quantitative framework

validated by real deployments:

COST REDUCTION

– Eliminate repetitive, rule-based cognitive work.

– Replace or augment call center, back-office, and compliance staff.

– Scale without proportional headcount growth.

– Voice AI agents deliver 60–80% cost reduction vs. human call centers.

– JPMorgan: ~30% reduction in consumer banking servicing costs.

REVENUE GROWTH

– 24/7 availability without shift premiums.

– Hyper-personalized customer experience at scale.

– Faster sales cycles through autonomous lead qualification.

– New market segments previously uneconomical to serve.

– Orange / Nexus: 50% conversion rate increase and $6M+ annual LTV from

a single customer onboarding agent.

PRODUCTIVITY & QUALITY

– PwC: quadrupled productivity in AI-augmented roles.

– Bessemer documents AI companies reaching $100M ARR in 18 months —

previously a 7-year journey.

– Sequoia: best AI startups earning “$1M+ in revenue per employee.”

– IBM AskHR: 11.5M interactions/year, 78% resolution rate, <5% human oversight.

STRATEGIC POSITIONING

– First-mover advantage in verticals where data accumulates as a moat.

– Bessemer: “Vertical AI companies have a unique opportunity to outperform

horizontal AI companies in the early days.”

– Deep integrations create high switching costs — the same dynamic that made

Salesforce and Workday so durable, but with AI compounding the advantage.

PART 6 | HOW NOT TO BUILD AN LLM WRAPPER STARTUP

Every major VC firm is now explicitly warning against the same failure mode:

building a thin wrapper around a foundation model and calling it a startup. The implication: the model is the commodity; the scaffolding, data, and

workflow depth is the moat.

The companies rising are building genuine system integration and domain depth. The ones falling are building polished chat interfaces on top of the latest API.

The specific moats that survive:

DOMAIN DATA MOATS

Build or accumulate proprietary domain data — clinical records (with consent),

legal precedent databases, agricultural sensor data, financial transaction

histories — that make your agent dramatically more accurate than any generic

model. This data cannot be replicated by an AI lab shipping a new model. Unstructured, multimodal enterprise data is the generational opportunity for startups that solve it.

DEEP WORKFLOW INTEGRATION

Embed your agent into existing systems of record — the EHR, ERP, TMS, CRM —

with bidirectional integration that is painful to rip out. The deeper the

integration, the higher the switching cost.

PROPRIETARY MEMORY AND LEARNED PREFERENCES

Build agent memory systems that accumulate and improve over time with each

customer — understanding specific processes, preferences, exceptions, and

edge cases. This institutional memory is a genuine moat, products that

get better the longer someone uses them.

VERTICAL-SPECIFIC ORCHESTRATION

Design multi-agent workflows encoding deep domain expertise — not just LLM

calls, but structured decision logic, regulatory rule engines, clinical

protocols, or financial models. This is the “agent harness” layer and is the core of a defensible application layer business.

TRUST AND COMPLIANCE AS A PRODUCT

In regulated industries, the compliance framework IS the product. Build HIPAA,

SOC 2, FedRAMP, or PCI-DSS certification into your architecture from day one.

OUTCOME-BASED PRICING

Companies that price on outcomes — cost per resolved ticket, cost per

closed loan, cost per passed audit — are structurally different businesses

from SaaS tool vendors. The pricing model signals the product architecture.

The question to ask: “What happens to this product when Claude 5 ships?” If

the answer is “it gets better because we plug in the new model as the reasoning

core while our data, integrations, and workflows remain intact” — that is a

real business. If the answer is “it becomes obsolete” — that is an LLM wrapper

on borrowed time.

PART 7 | REIMAGINING PRODUCT DELIVERY ACROSS VOICE, CHAT, AND IMAGE

VOICE-NATIVE AGENTS

Multilingual voice agents

THE BROWSER AS AGENT INTERFACE

MULTIMODAL INTELLIGENCE

Agents that can read medical images, analyze satellite farm photos, inspect

construction drone footage, or process financial documents add a perceptual

dimension unavailable to text-only systems.

UNIFIED AGENTIC INTERFACES

The endpoint is a single AI interface that a business deploys once — handling

voice calls, chat messages, image-based reports, and system actions with

consistent context, memory, and identity.

PART 8 | BENEFITS, RISKS, AND SURVIVAL ODDS: THE HONEST TABLE

DIMENSION BENEFITS RISKS

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

MARKET – 48% of global VC in 2025 went – Gartner: 40% of agentic

OPPORTUNITY to AI/LLM; agentic gets the deployments canceled

largest share (Tracxn: $24.2B by 2027 (rising costs,

cumulative, 143% YoY in 2026) unclear value, poor

– Bessemer: AI companies hit risk controls)

$100M ARR in 18 months vs – Sequoia warns of

7 years for legacy SaaS “delays” in both data

– Sequoia: “$0 to $1B club” center buildouts and

emerging in 2026 AGI timeline that may

slow enterprise adoption

COMPETITIVE – Vertical specialists show 3-5x – a16z: “New apps are

POSITION better retention than horizontal rising and falling very

tools (Bessemer) quickly” — the category

– Domain + compliance moat is highly dynamic

makes for defensible – Sequoia “innovator’s

enterprise contracts dilemma”: copilot

– Outcome-based pricing creates companies moving to

alignment with customer success autopilot “cut their

– Deep integrations = high own customers out of

switching costs doing it”

– First-mover data accumulation

compounds with scale

TECHNICAL – Modular, model-agnostic – LLM hallucination in

architecture protects against production remains real

model obsolescence – Sequoia: “agents still

– MCP/A2A open standards reduce fail — they hallucinate,

integration burden lose context, and

– Agent harness / scaffolding charge confidently down

is the real innovation layer exactly the wrong path”

– Observability tools maturing – “Agent-speed workloads

– Bessemer: private eval are massively concurrent,

frameworks unlock enterprise recursive, and bursty —

trust and 10x deployment current systems mistake them for attacks”

FINANCIAL – High margins on software- – Enterprise sales cycles

– delivered agent work remain long (6-18 months)

– Outcome-based pricing commands – Inference costs for

premium vs. seat-based SaaS complex multi-agent

– Bessemer’s Q2T3 archetype: systems are material

durable 60%+ gross margins – Bessemer warns of

– Sequoia: $1M+ revenue per “Supernova vs. Shooting

employee at best AI companies Star” trap — fast growth

with fragile retention and thin margins

REGULATORY & – Compliance as structural – GDPR, HIPAA, EU AI Act,

COMPLIANCE competitive advantage in and state AI legislation

regulated verticals are evolving rapidly

– Early movers shape with unresolved liability

compliance norms and become – Mandatory human oversight

the reference implementation requirements in high-

– Government deployments stakes domains add

create large, sticky contracts friction and cost

– Bessemer: trusted private evals – Data residency

as “deployment gate” = moat requirements complicate global scaling

TALENT – AI-native talent increasingly – Competition from

accessible globally OpenAI, Anthropic,

– a16z: most of the AI Google for top engineers

opportunity is outside Silicon – Rapid skill obsolescence

Valley — founding teams in requires continuous

traditional verticals have learning investment

the domain expertise VCs lack – Founder dependency risk

– $1M+ revenue per employee at in early-stage companies

best AI companies is real

SURVIVAL ODDS HIGHEST PROBABILITY LOWEST PROBABILITY

(2-5 YEAR – Vertical autopilots with – Thin LLM wrappers

HORIZON) domain data moats with no proprietary

– B2B with deep workflow data or integration

integrations and compliance – Generic horizontal

– Outcome-based pricing model copilots in markets

– Healthcare, legal, finance, where Big Tech has

logistics with regulatory native agents

barriers – Consumer-facing agents

– Companies acquired vs. competing directly

replaced (proprietary training with ChatGPT and

data is the acquisition signal) Gemini native features

BOTTOM LINE: Long-horizon agents have crossed the threshold from assistants into

autonomous workers — the era of passive chatbots is definitively over. Vertical

agentic AI companies with genuine workflow depth and domain expertise are

positioned to outperform generic horizontal platforms in both retention and

revenue durability. The category has not yet consolidated — massive white space

remains across every industry vertical. The startups that will define this era

are being founded right now, and the window to build a defensible position is

still open.

PART 9 | THE VC CONSENSUS: WHAT THE SMARTEST MONEY IS SAYING

This is no longer fringe optimism. The institutional consensus from the firms

that have collectively deployed hundreds of billions into technology is

remarkably unified:

A16Z (ANDREESSEN HOROWITZ)

– “AI is eating software.” The firm’s entire investment thesis has shifted.

– Big Ideas 2026: “Interfaces shift from chat to action.” Voice, agents,

and agentic execution define the next wave.

– Jennifer Li: Unstructured enterprise data is a “generational opportunity.”

– Seema Amble: The shift from copilots to end-to-end agents is inevitable

as model capability improves.

– Investment focus: Healthcare (40% of 2025 AI portfolio), infrastructure,

vertical autopilots. Key bets: Cursor, Harvey, Sierra, Hippocratic AI,

Ambience, ElevenLabs, Glean, Decagon.

SEQUOIA CAPITAL

– “Services: The New Software” — the most commercially actionable VC thesis

of 2026. A copilot sells the tool. An autopilot sells the work.

– “2026: This Is AGI” — long-horizon agents are functionally AGI; “2026 will

be their year.” The Don Valentine test: “Can you hire it?”

– Sonya Huang’s “Age of Abundance” thesis: AI makes once-scarce labor

available everywhere at near-zero cost.

– Key investments: Harvey ($200M, $11B valuation, March 2026), Glean, Cursor

(Anysphere), LangChain, Rogo.

– Market prediction: “The $0 to $1B club” emerging in 2026 for the best

agentic AI companies.

BESSEMER VENTURE PARTNERS

– State of AI 2025: “Three years after the AI Big Bang, early galaxies are

forming.” Vertical AI companies have a structural advantage.

– Two archetypes: “Supernovas” (fast growth, fragile) vs. “Shooting Stars”

(durable, 60%+ margins). Build for durable.

– MCP is “USB-C for AI.” The browser is the dominant agentic interface.

– Private evaluation frameworks will “10x enterprise deployment” in 2026.

– Prediction: incumbents will “aggressively acquire AI-native startups” —

plan your exit accordingly.

– Key investments: Anthropic, Cursor, SmarterDx, Fieldguide, Jasper, Plenful.

GENERAL CATALYST

– “Building the rails for the machine-to-machine economy.” (Marc Bhargava,

on Kite investment)

– Investment thesis: AI agents need identities, programmable governance, and

seamless payment flows to operate at internet scale.

– YC + GC backing of Nexus (March 2026) with the thesis: “Enterprises don’t

need another AI assistant — they need an AI agent that completes work

reliably and delivers measurable results from the start.”

– Orange deployment via Nexus: 50% conversion increase, $6M+ LTV,

10+ point increase in customer satisfaction. Four weeks to production.

– Key focus: Healthcare (Health Assurance Fund), enterprise SaaS, fintech.

Y COMBINATOR (WINTER 2026 DEMO DAY)

– “Agentic AI is not a feature, not a department — it is the operating layer

of the next enterprise stack.” (DynamicsFocus analysis)

– YC W26 themes: agentic cybersecurity, data infrastructure, vertical

automation. Companies achieving $1M+ ARR in under 8 weeks.

– The signal: institutional investors are “fighting over cap tables” for

agentic AI applications in specific verticals.

INSIGHT PARTNERS

– Led Wonderful AI’s $150M Series B (March 2026) with the thesis: “AI agents

are infrastructure, not features. They’re not add-ons to existing SaaS.

They’re platforms that replace workflows.”

– Led Legora’s $550M Series D at $5.55B valuation — alongside Bessemer, IVP,

and Index Ventures — confirming that legal AI autopilots command premium

multiples.

THE CONVERGENT MESSAGE:

Every one of these firms is saying the same thing with different words:

1. The model is infrastructure. The application layer is where founders win.

2. Vertical specialization beats horizontal generality.

3. Autopilots (sell the work) beat copilots (sell the tool).

4. Domain data, workflow integration, and compliance are the durable moats.

5. The window is open now. It will not be open forever.

THE CLOSING ARGUMENT: BUILD THE FUTURE, DON’T WAIT FOR IT

The real test for the agentic AI era: “Can you hire it?”

In 2023, you couldn’t. In 2024, you could hire it for narrow tasks. In 2026,

you can hire an agent that navigates a 31-minute recruiting search, manages

an end-to-end loan origination, handles clinical documentation across a health

system, or processes 11.5 million HR requests per year with 78% autonomous

resolution. That is a fundamentally different capability than a chatbot.

Every industry described in this article has a version of this question:

“What if the most capable, knowledgeable professional in this domain could

work 24/7, across every customer simultaneously, in any language, without

vacation, at a fraction of current cost, while continuously improving?”

That is not science fiction. That is the product description of a well-built

agentic AI autopilot in 2026.

a16z, Sequoia, Bessemer, and General Catalyst are not writing thought leadership

for entertainment. They are describing where their next billion-dollar returns

will come from. The founders who read those theses, understand their domain,

build the right architecture, and find the right enterprise buyers will join

them.

The companies that will define the next decade of enterprise software are being

founded right now. They are being built by founders who understand that the LLM

is infrastructure — and that the real value is in the domain expertise, the

workflow depth, the proprietary data, and the trust required to operate

autonomously in consequential business processes.

At IndusAgentAI, we believe agentic AI is not a threat to human economic activity.

It is the most powerful amplifier of human capability ever built. The founders

who deploy it responsibly — with genuine domain understanding, real architectural

depth, and honest attention to human impact — will create companies, careers,

and industries that we cannot yet fully imagine.

The window is open. Build something that matters.

ABOUT INDUSAGENTAI

IndusAgentAI.com is a platform dedicated to agentic AI innovation — exploring

the architecture, business models, and real-world deployment of autonomous AI

systems across industries. For founders, architects, and enterprise leaders

navigating the agentic AI transition.

PRIMARY VC SOURCES

a16z (Andreessen Horowitz):

– “Big Ideas 2026: Part 1 & Part 2” (December 2025) — a16z.com

– “Big Ideas 2026: The Agentic Interface” podcast (December 2025)

– “AI Speedrun: 14 Big Ideas for 2026” (December 2025)

– “The AI Application Spending Report” — Moore, Andrusko, Amble (2025)

– “Top 100 Gen AI Consumer Apps” — Olivia Moore, Anish Acharya (2025)

– “Humans Are for Ideas, AI Is for Execution” — Olivia Moore

Sequoia Capital:

– “2026: This Is AGI” (January 2026) — sequoiacap.com

– “Services: The New Software” (March 2026) — sequoiacap.com

– “AI in 2026: A Tale of Two AIs” (December 2025) — sequoiacap.com

– Sonya Huang, AI Ascent 2025 keynote: “The Age of Abundance”

– “AI in 2025: Building Blocks Firmly in Place” (December 2024)

Bessemer Venture Partners:

– “The State of AI 2025” — Dholakia, Droesch, Moore (August 2025) — bvp.com

– “Roadmap: AI Systems of Action” — bvp.com

– “Part I & II: The Future of AI Is Vertical” — bvp.com

– “Bessemer’s AI Agent Autonomy Scale” — bvp.com

– “State of Health AI 2026” — bvp.com

General Catalyst:

– “Our Investment in Kite” — generalcatalyst.com (September 2025)

– Nexus seed investment announcement (March 2026)

– Hemant Taneja: “Applied AI and Resilience” investing thesis

Additional VC & Research Sources:

– Insight Partners: Wonderful AI Series B analysis (March 2026)

– Y Combinator: Winter 2026 Demo Day analysis (April 2026)

– Prosus / Dealroom: “The Rise of the Agentic Workforce” (2025)

– Tracxn: Agentic AI Sector Report (April 2026)

– Kore.ai: Agentic Architecture — Blueprint for Intelligent Enterprise (2026)

– Prosus / Dealroom.co — “The Rise of the Agentic Workforce” (2025)

– Tracxn Agentic AI Sector Report (April 2026)

– Goldman Sachs Research — “How Will AI Affect the Global Workforce?” (2025)

– World Economic Forum — Future of Jobs Report 2025

– McKinsey Global Institute — Scaling Agentic AI with Data Transformations

– Deloitte Insights — Autonomous Generative AI Agents (2025)

– Bain & Company — The Three Layers of an Agentic AI Platform (2026)

– ITIF — “AI’s Job Impact: Gains Outpace Losses” (December 2025)

– ILO — World Employment and Social Outlook 2025

– Google Cloud — Agentic AI Architecture Components Documentation

– Neo4j — Agentic AI Architecture: Patterns and When to Use Them

– Akka — Agentic AI Frameworks for Enterprise Scale: A 2026 Guide

– PwC — 2025 Global AI Jobs Barometer

– StartUs Insights — 10 AI Agent Startups to Watch in 2026

– Presta — AI Agent Startup Ideas That Made $1M+ in 2026

– Linas Beliūnas Newsletter — Agents 20: Top AI Agent Startups of 2025

– Gartner — Enterprise AI and Agentic Adoption Forecasts

– Nextgov/FCW — 2026 Is Set to Be the Year of Agentic AI (December 2025)

– SSRN — AI Job Displacement Analysis 2025-2030 (Nartey, 2025)